Here’s a bright, big-picture rundown of the latest moves to make India a semiconductor power hub—plus what it could mean for the economy next. (Updated: Sep 4, 2025 )

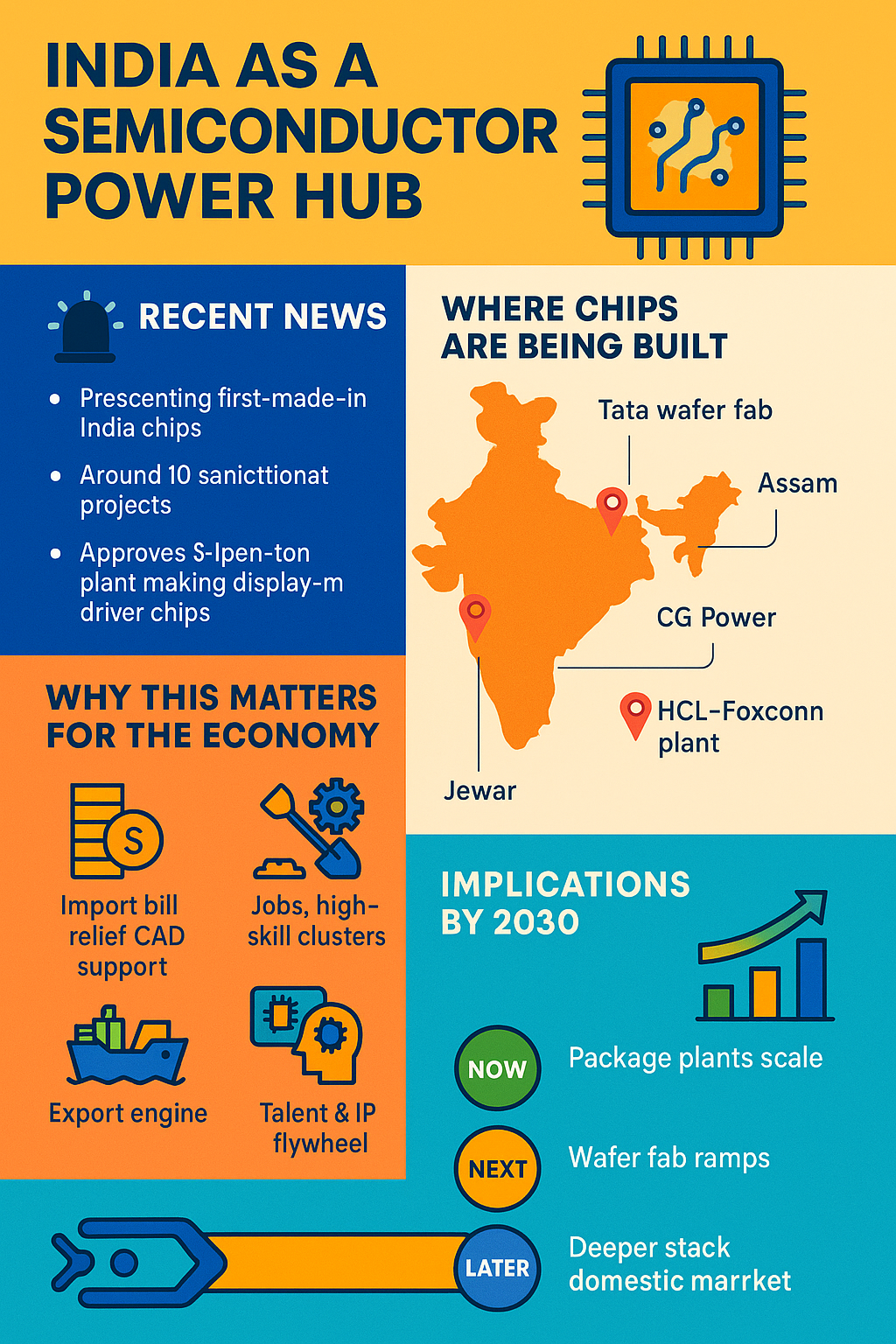

“First made-in-India chips” presented at Semicon India 2025 (Sep 2, 2025). Govt announced 12 MoUs (talent, camera modules, MEMS mics, packaging, design IP access) and teased ISM 2.0 + a $1B Deep Tech Alliance to fund frontier tech. (Press Information Bureau)

4 more projects approved (Aug 12, 2025)—India now counts ~10 sanctioned semicon projects under ISM. (India Briefing)

HCL–Foxconn JV approved (May 14, 2025) near Jewar, UP: 20,000 wafers/month making display-driver ICs; the 6th ISM unit. (Press Information Bureau, Reuters)

Micron (Sanand) hits clean-room validation (Jun 2025)—a key step to ramp its memory ATMP. (The Economic Times)

CG Power (Sanand) OSAT push gathering steam; investor coverage & launch updates in late Aug/Sep. (The Economic Times)

Tokyo Electron (chip-equipment major) planning offices in Dholera & Assam to support Tata’s fab/OSAT. (The Economic Times)

States joining the party: Odisha signed ₹2,655 crore worth of MoUs to seed PCB/semicon ecosystem & training tie-ups. (The Times of India)

Tata–PSMC wafer fab (Dholera, Gujarat)—₹91,000 cr, 50k wafers/month (28 nm PMICs, DDIs, MCUs/HPC logic). Approved Feb 29, 2024; ecosystem build-out (housing, materials supply, equipment presence) accelerating. (Press Information Bureau, The Economic Times)

Tata OSAT (Morigaon, Assam)—₹27,000 cr, advanced packaging (flip-chip, SiP). (Press Information Bureau)

CG Power + Renesas + Stars (Sanand, Gujarat) OSAT—₹7,600 cr; pilot/launch activity reported; brokerage upgrades reflect confidence. (Press Information Bureau, The Economic Times)

Kaynes Semicon (Sanand)—Cabinet nod Sep 2, 2024; 6 crore chips/day capacity (discrete/analog segments). (Press Information Bureau)

Micron ATMP (Sanand)—phase-wise ramp; clean-room validation in Jun 2025 (official plan had late-2024 ops start, then gradual ramp). (Micron Technology, The Economic Times)

HCL–Foxconn (Jewar, UP)—36 mn DDICs/month design output; 20k wafers/month; commercial ops targeted by 2027. (Press Information Bureau, Reuters)

Policy backbone: ISM offers up to 50% fiscal support for fabs, displays, compound semis & ATMP/OSAT on a pari-passu basis—critical to closing India’s cost gap. (acma.in, Press Information Bureau)

1) Import bill relief & CAD support

India imported 18.43 billion chips in FY24 (₹1.71 lakh cr). As ATMP/OSAT and (later) wafer fabs localize value-add, electronic imports should soften at the margin, improving current-account dynamics—especially in smartphones, autos, and industrials. (The Economic Times)

2) Jobs & high-skill clusters

The Feb 2024 trio alone projected ~20k direct + ~60k indirect jobs; with new approvals, cluster effects in Sanand–Dholera, Assam, YEIDA/Jewar could multiply roles across chemicals, specialty gases, ultrapure water, HVAC, tooling, facilities, logistics, and EDA/design services. (Press Information Bureau)

3) Export engine

Plants like Micron ATMP and DDI lines are built for global demand; expect exports of memory packages and display drivers once yields stabilize, adding a new tech-manufacturing export lane alongside mobiles. (The Economic Times)

4) Upgrading value chains

MoUs at Semicon India 2025 aim to localize camera modules, MEMS mics, secure ID chips, and to expand materials/equipment presence (e.g., Merck chemicals, Tokyo Electron support)—raising domestic content share and resilience. (Press Information Bureau, The Economic Times)

5) Talent & IP flywheel

India already houses ~20% of the world’s chip-design engineers; DLI/Chip-to-Startup + 78 universities on advanced EDA tools deepen the design-to-product pipeline. (The Times of India, Press Information Bureau)

6) Market pull

India’s chip market is projected to reach $100–110 bn by 2030, providing strong local demand to anchor fabs/OSAT before export scale kicks in. (ETManufacturing.in, DD News)

Time-to-yield: first-gen fabs/OSAT face yield & ramp risks; schedules can slip with supply-chain bottlenecks or tool qualifications (common in greenfield sites).

Tech node choices: starting at 28 nm & power/analog is pragmatic; moving to <14 nm needs deeper EUV ecosystem, higher capex, and export-control navigation.

Cyclicality: global memory/logic cycles can swing pricing; subsidies must bridge downturns without distorting incentives.

Power, water, and materials reliability: sustained grid stability, UPW, specialty gases/chemicals and waste handling are non-negotiable for yields.

Project churn: some proposals have paused/withdrawn (e.g., Adani–Tower paused; Tower reportedly exited an earlier fab plan), underlining execution risk. (Reuters, EENews Europe)

NOW (2025): 🟩 Package & Test at scale—Micron, CG Semi, Kaynes lines; supply-chain on-shoring for materials/equipment; state MoUs expand the funnel. (The Economic Times, The Times of India)

NEXT (2026–27): 🟨 Dholera wafer fab ramps, HCL–Foxconn DDIs, more OSAT capacity; expect first meaningful chip exports and import substitution in autos/consumer. (Press Information Bureau)

LATER (2028–30): 🟦 Deeper stack—more nodes (power/analog & specialty), SCL Mohali modernization, stronger design-to-manufacture linkages, and $100B+ domestic market as anchor. (DIGITIMES Asia, ETManufacturing.in)

Feb 29, 2024: Cabinet OKs Tata–PSMC fab (Dholera), Tata OSAT (Assam), CG–Renesas OSAT (Sanand); “start construction in 100 days.” (Press Information Bureau)

Sep 2, 2024: Kaynes Semicon unit approved (Sanand). (Press Information Bureau)

May 14, 2025: HCL–Foxconn JV approved (Jewar). (Press Information Bureau)

Jun 2025: Micron Sanand clean-room validation. (The Economic Times)

Aug 12, 2025: 4 new ISM projects approved (total ~10). (India Briefing)

Sep 2, 2025: Semicon India 2025: first chips showcased + 12 MoUs + ISM 2.0 signals. (Press Information Bureau)

I

Continue With Google

Continue With Google  Current affair

Current affair

Business

Business