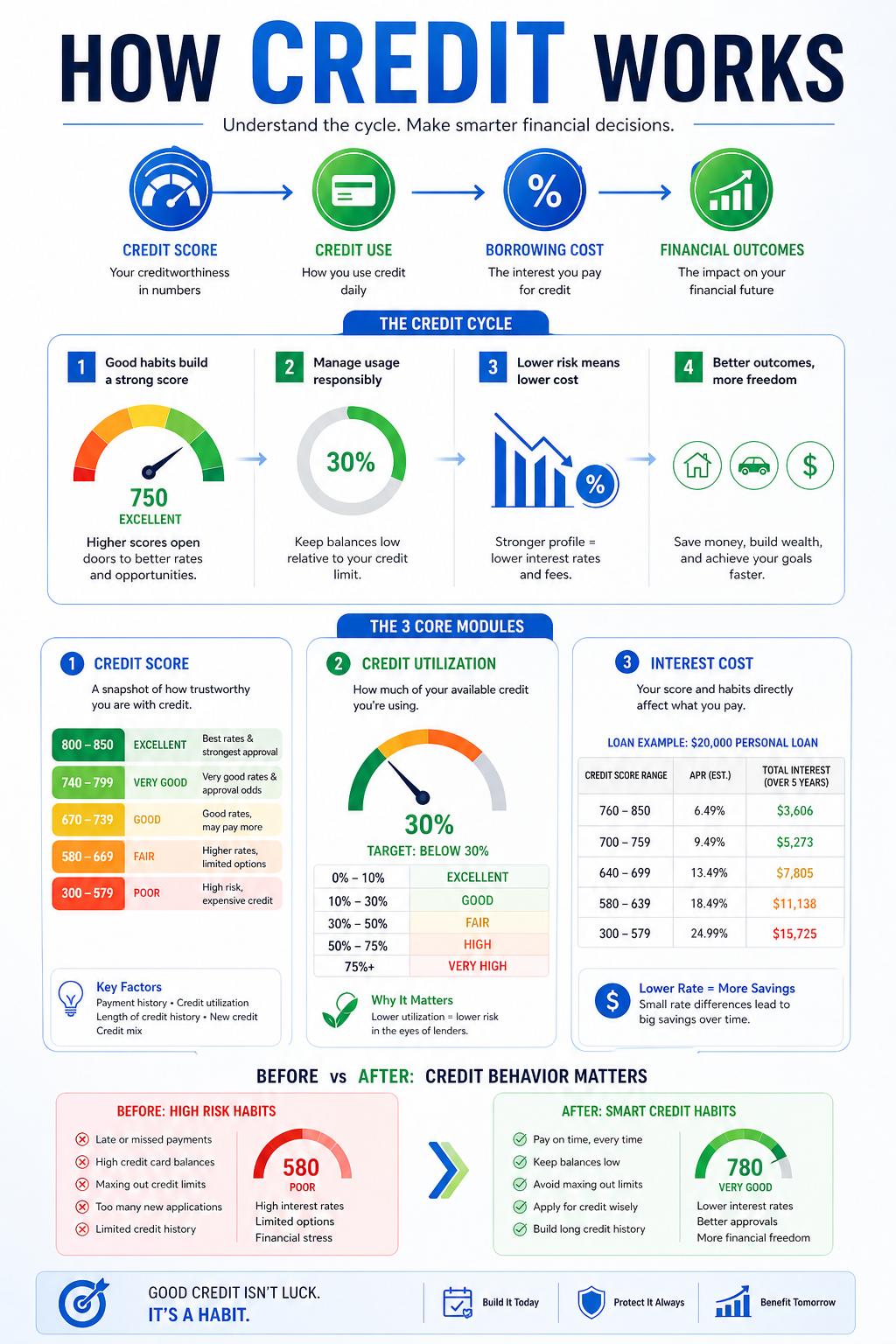

A credit score is a numerical indicator used by lenders to assess how reliably a person manages borrowed money. Although many people treat it as mysterious or overly technical, the logic behind a credit score is relatively straightforward: it attempts to estimate risk.

A higher credit score generally suggests lower lending risk, which may improve access to loans, credit cards, or favorable interest rates. A lower score may increase borrowing costs or reduce approvals.

Several factors commonly influence a credit score.

1. Payment History

This is often one of the most important factors. Consistently paying bills or loan installments on time signals financial reliability. Missed or delayed payments can negatively affect a score.

2. Credit Utilization

This refers to how much of available credit is being used. For example, using a very large portion of a credit card’s limit may suggest financial strain, even if payments are being made.

3. Length of Credit History

Longer credit histories can help lenders evaluate patterns over time. This is one reason old well-managed accounts may contribute positively.

4. Credit Mix

Having only one type of borrowing is different from managing different forms of credit responsibly. Some scoring models consider this.

5. New Credit Inquiries

Frequent applications for new credit in a short period can sometimes be interpreted as higher risk.

A common misconception is that building credit means carrying debt. In reality, credit health is often more closely tied to responsible use than to borrowing heavily.

Understanding credit scores matters because they can affect financial flexibility over time. They often influence not only whether credit is available, but how expensive that credit becomes.

A useful way to think of a credit score is not as a judgment, but as a behavioral signal built from financial habits.

Continue With Google

Continue With Google  Account and Finance

Account and Finance

Education

Education